How should the rental or usage fees for shared facilities or equipment between related parties be determined under the arm's length principle?

In Stock

$34.99

$29.99

Shipping and Returns Policy

- Deliver to United States » Shipping Policy «

- - Shipping Cost: $5.99

- - Handling time: 2-3 business days

- - Transit time: 7-10 business days

- Eligible for » Returns & Refund Policy « within 30 days from the date of delivery

Find similar items here:

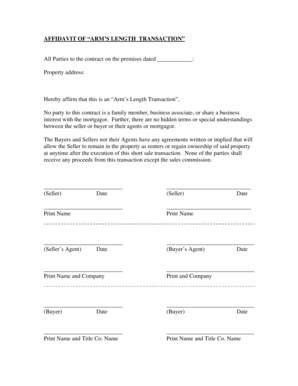

what is a non arm's length transaction

- How can companies integrate ESG considerations into their transfer pricing policies for non-arm's length transactions? What are the specific challenges in determining the arm's length price for transactions involving intellectual property created through collaborative efforts between related parties?

- What are the transfer pricing considerations for transactions involving research and development activities conducted collaboratively by related parties? How should the costs, risks, and rewards of collaborative R&D be allocated between related entities for transfer pricing purposes?

- What are the challenges faced by developing countries in administering transfer pricing rules for non-arm's length transactions? How does the United Nations Model Tax Convention address transfer pricing issues in non-arm's length transactions?

- How should government incentives be treated in transfer pricing analysis?

- How does Country-by-Country (CbC) reporting relate to non-arm's length transactions?

- What are the time limits for seeking competent authority assistance?

- How do tie-breaker rules in tax treaties affect the determination of tax residency in the context of non-arm's length transactions? What are the transfer pricing implications of permanent establishment rules under tax treaties?

- What are the key characteristics of a non-arm's length transaction?

- How should the rental or usage fees for shared facilities or equipment between related parties be determined under the arm's length principle?

- What are the transfer pricing considerations for business restructurings involving related parties? How are the tax consequences of cost contributions to develop intangible assets between related parties determined?

-

Next Day Delivery by USPS

Find out more

Order by 9pm (excludes Public holidays)

$11.99

-

Express Delivery - 48 Hours

Find out more

Order by 9pm (excludes Public holidays)

$9.99

-

Standard Delivery $6.99 Find out more

Delivered within 3 - 7 days (excludes Public holidays).

-

Store Delivery $6.99 Find out more

Delivered to your chosen store within 3-7 days

Spend over $400 (excluding delivery charge) to get a $20 voucher to spend in-store -

International Delivery Find out more

International Delivery is available for this product. The cost and delivery time depend on the country.

You can now return your online order in a few easy steps. Select your preferred tracked returns service. We have print at home, paperless and collection options available.

You have 28 days to return your order from the date it’s delivered. Exclusions apply.

View our full Returns and Exchanges information.

Our extended Christmas returns policy runs from 28th October until 5th January 2025, all items purchased online during this time can be returned for a full refund.

No reviews yet. Only logged in customers who have purchased this product may leave a review.